The Bottom Line

Small business is important to Central Oregon, and to Mid Oregon. Find tips and resources for business, and information about Mid Oregon’s commercial services and business members.

Caller ID Spoofing: Don’t Hang On, Hang Up

As with many local financial institutions, we are hearing increasing reports of fraudulent phone calls and text messages claiming to be from Mid Oregon..

Many of these calls even display accurate Mid Oregon phone numbers on caller ID. Scammers try to convince members that fraud is happening on their accounts and ask them to provide passwords, login information, card numbers, and even PIN numbers.

To help you avoid falling victim to these scams, we will discuss spoofing, provide prevention tips, and explain what to do if you suspect you have been scammed.

Please remember that Mid Oregon will NEVER ask you for your Digital Banking login credentials and passwords, PINs, SSNs, or credit and debit card numbers. If you receive one of these calls or messages, contact Mid Oregon at 541-382-1795. (DO NOT click on links in text messages!). More details on our Fraud Prevention page.

What Is Spoofing?

Spoofing is when a caller deliberately falsifies the information transmitted to your caller ID display to disguise their identity. Scammers often use “local “neighbor” spoofing so it appears that the call is coming from a local number, or spoof a number from a company that you may already know and trust. If you answer, they use scam scripts to try to steal your money or valuable personal information.

How to avoid spoofing?

- It can be difficult to distinguish a spoofed call from a genuine one. Be extremely careful about responding to any request for personal identifying information (watch video).

- It is best not to answer calls from unknown numbers. If you do pick up such a call, hang up immediately. If you receive a call from a person or bot that asks you to press a button to stop getting phone calls, it’s a good idea to hang up. Scammers often use this trick to identify potential victims.

- Let it go to voicemail. If you have a voicemail account, set a password to protect it. Some voicemail services allow anyone who calls from your phone number to access your voicemail, so it’s essential to set up a password to prevent hackers from gaining access.

- Do not answer any questions, especially those that can be answered with “Yes” or “No.”

Under no circumstances should you provide personal information, such as account numbers, Social Security numbers, mother’s maiden names, passwords, or any other identifying information, in response to an unexpected call or if you are even slightly suspicious. If you receive one of these calls or messages from Mid Oregon, please contact us immediately at 541-382-1795. (DO NOT click on links in text messages!).

- If someone claims to represent a company or a government agency calls you, hang up and call the phone number on your account statementor on the company’s or government agency’s website to verify the authenticity of the request. Legitimate sources generally send written statements before calling, particularly if the caller is requesting a payment.

- Be cautious if the person on the phone pressures you for information immediately.

- Talk to your phone company about call-blocking tools and investigate apps that you can download to your mobile device. The FCC allows phone companies to block robocalls by default based on reasonable analytics. You can learn more about robocall blocking at fcc.gov/robocalls.

How do I report suspected spoofing?

If you suspect your caller ID information has been falsified, you can file a complaint with the FCC:

▪ Online at https://consumercomplaints.fcc.gov.

▪ By phone: 1-888-CALL-FCC (1-888-225-5322); TTY: 1-888-TELL-FCC (1-888-835-5322); ASL: 1-844-432-2275.

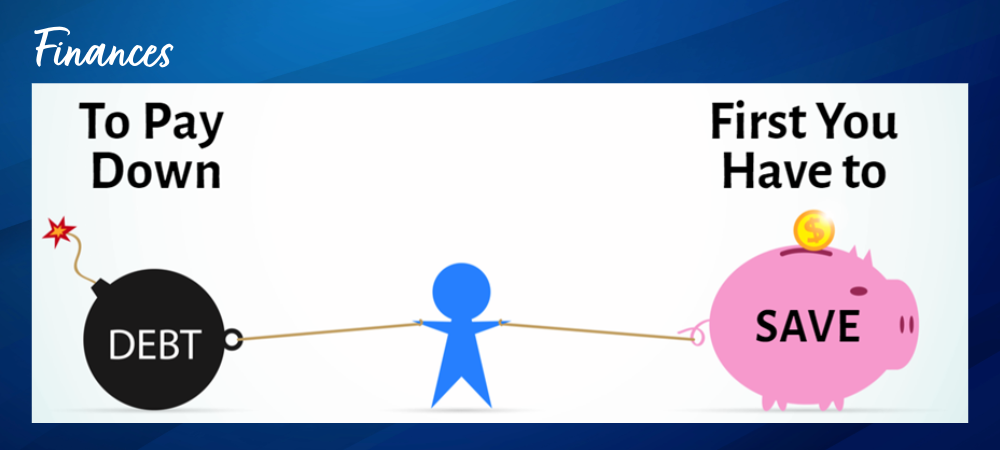

Savings vs. Paying Down Debt

Are you torn between saving money and paying down debt?

While paying down debt is crucial for your financial health, saving money is equally—if not more—important.

Many people’s first instinct to paying off debt is to withdraw from their emergency fund, retirement fund, or other savings accounts. The logic behind this is that your debt is likely costing you more money every month than your savings is earning you.

However, this strategy could actually lead to more debt in the long run. Crazy, right? But, think about it—if you’re neglecting your savings account and using all your extra funds to pay off your loans, what will happen if an emergency comes up, such as unexpected car repairs, vet bills, or even job loss?

We get it, life happens, but if you don’t have a savings account, you might find yourself in a difficult situation where you have to rely on your credit card to cover unexpected expenses. This can be frustrating, especially if you’ve been working hard to pay off your debts.

Breaking the cycle

1. The first step is to stop using your credit cards and adding to your debt.

2. Instead, set a realistic goal for your savings account that would cover most emergencies, such as $500.

3. While you’re building up your savings to reach that goal, make sure to pay at least the minimum payments on your loans.

4. Once you’ve reached your $500 savings goal, you can start dedicating more money to paying down your debt.

5. If an emergency comes up and you have to dip into your savings, don’t worry. Just switch back to paying the minimum on your debt and put any extra money into your savings to build it back up again.

By following these steps, you can build a safety net and get your finances under control.

Make savings a priority

Set up a specific but realistic goal. If you are receiving a tax refund this year, use part of that money to give yourself a head start. Use a savings goal calculator, such as Mid Oregon’s Savings Goals tool in Digital Banking, to see how much you’d have to save each month. Or, explore the variety of savings options Mid Oregon offers:

- Share Certificates—Enjoy higher returns on your investments and keep your money safe and local. We have amazing rates right now so take advantage of our latest special.

- High Yield Savings Accounts—Savings account with a variable dividend rate that increases as the balance increases (minimum balance $1,000).

- IRA Accounts—Build your future and your nest egg faster with attractive rates of return and choices to fit every budget and savings goal.

- Saver’s Club Certificate—Set your goal and the amount you want to save every month. It’s ideal for saving for something special or not being caught short during the holidays.

Saving sufficiently for the future—whether that’s tomorrow or years from now—is crucial. From regular savings and high-yield savings accounts to share certificates, Mid Oregon offers a variety of savings options and strategies to cater to your unique needs.

Don’t let the burden of debt get in the way of your savings goals. Mid Oregon is here to help you navigate through the complexities of managing your finances.

Smart Money Moves: Making the Most of Your Extra Cash

As the saying goes, “money doesn’t grow on trees.” So, when you happen to find yourself with some extra funds, it’s important to make the most of them.

Whatever the source of your unexpected windfall—a bonus from work, a tax refund, an inheritance, or just a bit of budget surplus—it can be exciting, and splurging can be tempting.

While nothing is wrong with treating yourself, it pays to pause and consider ways to leverage your extra cash to improve your financial goals.

Prioritize Your Financial Goals

Take some time to think about your own financial goals and rank them in order of importance. Once you have a good understanding of your goals, explore ways to allocate those extra funds, such as:

- Pay off debt and improve your credit score.

- Save for emergencies and unexpected expenses.

- Invest in your future and reach your financial goals.

- Create a sense of financial security and stability.

Pay off high-interest debt

Although this may not be the most exciting option, if you carry any high-interest debt, such as credit card debt or a personal loan, it’s important to prioritize paying it off. Paying down these types of debts can save you money in the long run since they can quickly accumulate and become a financial burden.

Start by paying off the debt with the highest interest rate first, saving you the most money in interest payments. If you have multiple high-interest debts, consider consolidating them into one lower-interest loan to make it easier to manage and pay off.

Build an emergency fund

Having an emergency fund is crucial for financial stability. Without relying on credit cards or loans, it can help cover unexpected expenses, such as car repairs or medical bills.

Experts recommend saving at least three to six months of living expenses in an emergency fund. If you don’t have one, use your extra funds to build one. Consider opening a high-yield savings account to earn interest on your emergency fund.

Invest in a Retirement Account

It’s never too early to start saving for retirement. If your employer offers a 401(k) or similar retirement plan, take advantage of it and contribute as much as possible. If your employer doesn’t offer a retirement plan, consider opening an individual retirement account (IRA).

Retirement accounts allow you to save for the future while providing tax benefits. Plus, the earlier you start saving, the more time your money has to grow.

Invest in yourself

Investing in yourself can also be a smart way to allocate extra funds. This can include furthering your education, attending conferences or workshops, or even starting your own business. Think about your long-term career goals and how investing in yourself can help you achieve them. This can lead to higher earning potential and financial stability in the future.

Splurge a little

There are several financially prudent ways to spend extra cash, but it is okay to spend some of it on something fun, too. Just take the time to consider your financial needs and goals and ensure your purchases align with them.

Putting the money into a savings account while deciding how to spend is a smart strategy. You may treat yourself with a small part of it, but use the rest to pay down debt, boost your investments, or keep saving.

Final thoughts

Getting the most out of your extra funds is key to financial stability and growth. By paying off debt, building an emergency fund, investing in retirement, and investing in yourself, you can make the most of your money and set yourself up for financial success.

Remember to consider your financial goals, risk tolerance, time horizon, and personal values when deciding where to allocate your money. And don’t be afraid to seek the advice of a financial advisor to help you make the best decisions for your financial future.

Whether it’s an unexpected windfall or not, being thoughtful with money is always the best way to achieve your financial goals.