The Bottom Line

Small business is important to Central Oregon, and to Mid Oregon. Find tips and resources for business, and information about Mid Oregon’s commercial services and business members.

Message from the CEO: Protecting your data is Mid Oregon’s top priority

We’ve all been through it. Having your private personal data compromised is frightening.

That’s why at Mid Oregon Credit Union, we believe protecting the privacy and security of our members’ accounts is our most important responsibility.

Acting Quickly

When we discover a data breach, we act immediately to change account numbers and issue new credit and debit cards for affected members. Additionally, we pursue cyber criminals through available legal channels. But, under current regulations, we are not allowed to tell you which organization is responsible for the breach.

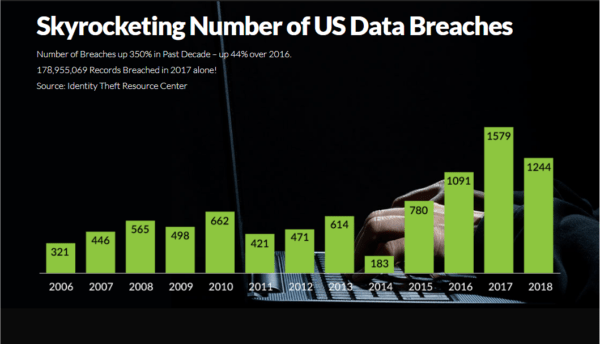

Having your personal financial data stolen is enough of a burden. You shouldn’t have to worry about who is going to clean up the mess and pay the bills for the fraud. The problem keeps getting worse.

2018 Data Breaches

More than 1,200 data breaches occurred in 2018, exposing more than 197 million data records—a 126% increase over 2017. The number of records breached in 2018 is likely higher since only half of the breaches reported included the number of records exposed. Read more about the problem here.

Most of us assume the organization responsible for the breach pays the costs since their security failures caused the theft of your data. Sadly, that’s not how it works.

Credit unions like Mid Oregon bear the brunt of the expenses after a data breach, even though we (and members like you) had nothing to do with it.

Credit Unions Pay the Price

To give you one example, after the Target breach, credit unions were left on the hook for $30.6 million and credit unions reissued 4.6 million credit and debit cards.

Right now, organizations responsible for these breaches can shift most of the costs of their data breaches to others. Because we are not-for-profit cooperatives owned by our members, you ultimately foot the bill to clean up their mess. There is no incentive for the organizations that allowed the breaches to spend the time and money to increase their data security. That’s wrong for consumers and bad for our economy.

Calling on Congress!

That’s why Mid Oregon and other credit unions across the country are working together to improve protections for credit union members who are victims of data breaches.

We’re calling on Congress to step up and protect credit union members.

I hope you’ll consider lending your voice to this important effort. Please click on this link to learn more about the problem and send an e-mail to your U.S. Representative and U.S. Senators.

Thank you for making your voice heard on this important subject on behalf of your fellow consumers.

Sincerely,

Bill Anderson

CEO, Mid Oregon Credit Union

PS—Data breaches are scary and inconvenient, but Congress can protect consumers like you. To find out more, visit StoptheDataBreaches.com.

Tell-A-Friend About Checking and Win!

Tell-A-Friend About Checking

And Get a chance to win!

Good friends tell each other about great deals. And, when you Tell-A-Friend about Mid Oregon checking accounts, you both earn a reward—and chances to win. When your friend opens a Mid Oregon Credit Union checking account, we’ll buy back their old debit cards and checks for up to $10, and enter them to win a branch Grand Prize!

What do you get? A $10 gift card and a chance to win too! From now through September 30, referrals made through our Tell-A-Friend program will enter the referrer to win a Traeger Ranger tabletop grill, valued at $399.

Traeger Ranger Pellet Grill Prize

The Traeger Ranger Pellet grill can go where you go, to the great outdoors or a great friend’s house. Featuring Traeger’s Digital Arc controller, the Ranger gives you precise temperature control with an added Keep Warm Mode to make sure your food is ready to eat whenever you are. Some quotes from Traeger’s website about the grill:

“The size is perfect for 2-4 people and roomier than I expected as I was able to smoke a 12 lb beef brisket in it and it came out amazing for a first go on the Ranger.” “Space saver on a patio (because of no legs). Fits perfect on top an outdoor refrigerator or counter top. Price is great value. Cooking surface big enough for three couples.” “As long as you have a power source this thing will go anywhere you can go. Because of it’s size it heats up fast and barely uses any pellets so you don’t have haul extra bags around.”

Free Checking Account and More!

Through 10/11/19, the person referred who opens a new checking account at Mid Oregon Credit Union is automatically entered to win a $250 Sportsman’s Warehouse gift card drawn for each of our seven branches. After 10/11, there will be another prize opportunity. They will get a great free checking account, with no minimum balance requirement or monthly service fees. Every new personal checking account at Mid Oregon Credit Union includes a Free Debit Card, Free Online banking with Free eBillPay, Free Mobile Banking plus Mobile Deposit, Free eStatements with online check images. Plus, we will buy back your debit cards and unused checks from another financial institution. Learn more about Mid Oregon Checking Accounts today!

Just visit refer.midoregon.com to get started, and Tell-a-Friend about checking! You can refer as many friends as you like (and earn as many gift cards as you want). You don’t even need to have a Mid Oregon Checking account—although, why would you miss out?

Tell-a-Friend Drawing Rules

Tell-a-Friend Drawing Rules: No purchase necessary to enter or win a prize. Must be 18 years or older. Entries accepted through September 30, 2019. No cash equivalent, substitution or transfer of prize permitted. One drawing entry per referrer. Other restrictions apply; see a Mid Oregon Credit Union Associate for details.

Presidents Message: Directed to serve our members and community

The Direction of Our Institution

Quite often, you hear us mention that Mid Oregon is member-owned and guided by a democratically-elected, all-volunteer Board of Directors. Our Board consists of

members who meet regularly to determine the direction of our institution.

These folks help provide me and the rest of the Mid Oregon Credit Union team with a set of guiding concepts to shape the work we do. Unlike many organizations that focus on activities, we focus on the end results. That’s why the board has developed a set of “Ends” Statements—a list of things that we are accountable for accomplishing as an organization.

Mid Oregon “Ends” Statements

You probably wouldn’t be surprised to know that our first few Ends Statements refer to providing affordable, convenient financial solutions to our members and member-businesses, and ensuring Mid Oregon is a safe, stable, and secure financial partner. Being here for your financial needs is our primary purpose.

But we have a couple others that might not be as obvious. The first is to increase the financial literacy of our members and the community. Recently, we’ve accomplished this through hosting a “Bite of Reality” budgeting simulation at La Pine High School, and scheduling a wide array of financial workshops.

Making a Difference in Our Communities

The other is making a difference in our communities. Whether it’s our support of the upcoming Duck Race, hosting this month’s Supplies 4 Schools branch drives,

pledging $50,000 to the St. Charles Tower expansion, or sponsoring Free Family Days at the High Desert Museum, we look for ways to collaborate with local partners to

make life better for everyone in our communities.

We are accomplishing great things together. Thank you for your membership.

Bill Anderson

CEO, Mid Oregon Credit Union